Title insurance feels expensive for one reason more than any other: you pay a meaningful amount all at once, right when you are already writing checks for everything else.

That sticker shock is real. But the number only makes sense once you understand what the premium is actually covering, what part of your closing bill is insurance versus settlement work, and why this is nothing like your auto or homeowners policy.

In Virginia, Maryland, and DC, buyers usually see title insurance for the first time on a loan estimate or closing disclosure and think the same thing: Why am I paying this much for something I may never use?

Here is the plain-English answer.

Why the number feels bigger than buyers expect

Title insurance is typically a one-time premium paid at closing. That matters.

Most insurance products are spread out over time. You pay auto insurance monthly. You pay homeowners insurance yearly. You may never think too hard about the full multi-year total because the cost is broken into smaller payments.

Title insurance is different. The premium shows up all at once, in the middle of a much larger closing statement, and that makes it feel outsized.

On a $600,000 purchase, the title insurance line item may look large compared with recording fees or courier charges. But that does not mean it is overpriced. It means you are buying protection for one of the largest financial transactions of your life in a single payment.

What you are actually paying for

A lot of buyers assume title insurance is just a paper policy. It is not.

The premium reflects the risk that someone could later challenge ownership or uncover a defect tied to the property's legal history. Before the policy is even issued, the title company has to do the work that makes closing possible.

That usually includes:

- Searching public records for deeds, liens, judgments, releases, and tax issues.

- Reviewing the chain of title to confirm the seller can legally convey the property.

- Identifying problems that must be resolved before closing.

- Coordinating with lenders, agents, attorneys, HOAs, and payoff departments.

- Preparing for the actual settlement and recordation process.

- Standing behind the policy if a covered issue later surfaces.

In other words, you are not just buying a document. You are paying for risk evaluation, defect clearance, closing coordination, and long-tail protection.

Why title insurance is not priced like other insurance

This is the part most people miss.

With auto or health insurance, the carrier expects frequent claims across a large pool of policyholders. Pricing reflects recurring exposure.

With title insurance, the model is different. Much of the cost sits up front because the title company and underwriter are trying to catch problems before the policy is issued. The work happens early, not after a claim.

That is why title insurance often looks expensive relative to the number of claims consumers hear about. The product is designed around prevention first, coverage second.

If the title search catches an unreleased lien, a probate problem, a boundary dispute, or an old deed issue before closing, that problem can often be fixed before it becomes your problem. That prevention work is part of the value.

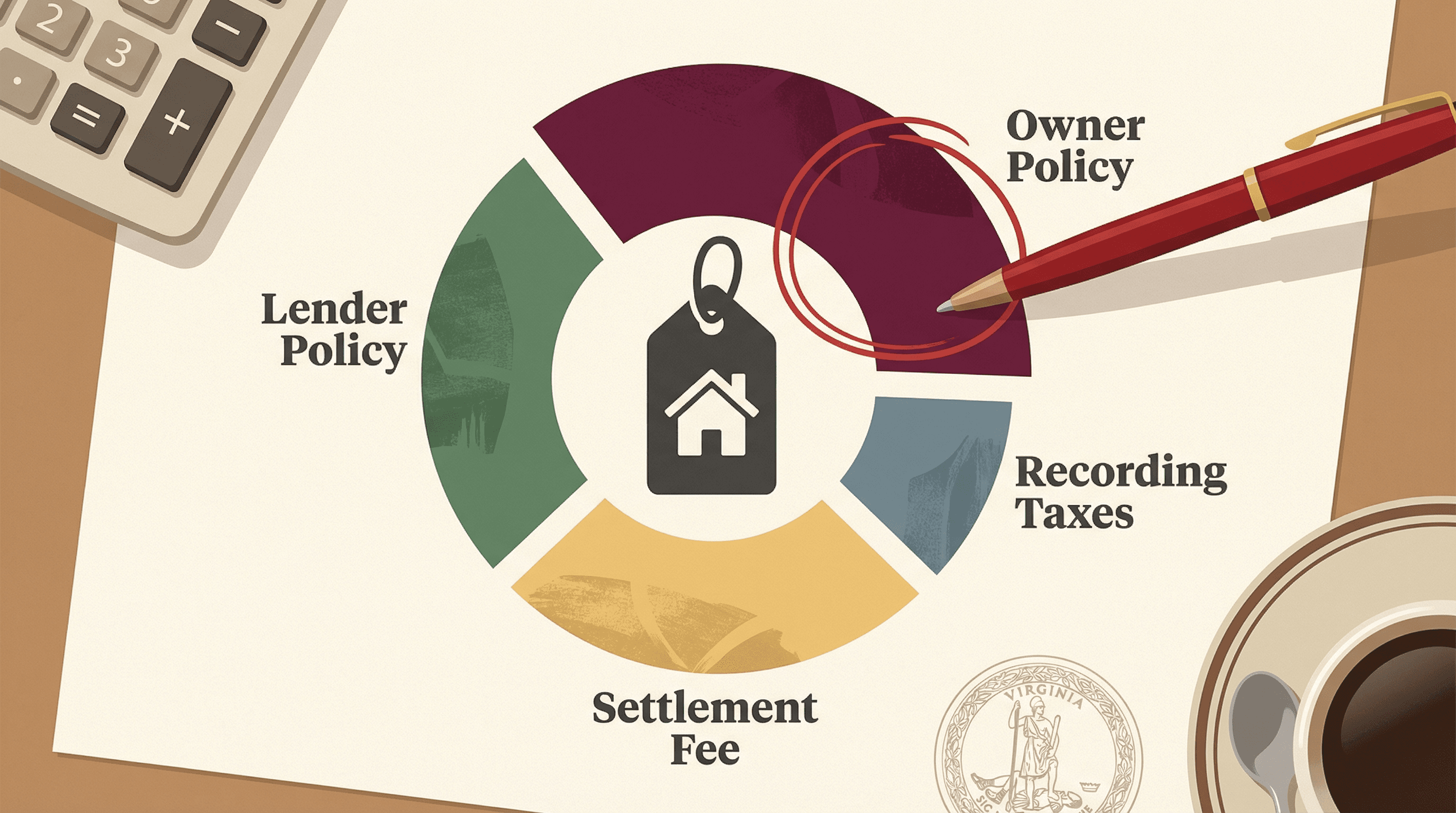

The insurance premium is not the whole title bill

Another reason buyers get confused: they lump every title-related charge into one bucket.

Some of your closing costs are actual insurance premiums. Some are settlement or escrow fees. Some are recording and transfer charges imposed by the jurisdiction.

| Cost type | What it covers | Who controls it |

|---|---|---|

| Owner's title insurance premium | Protects the buyer's ownership interest | Filed/regulated or underwriter-based pricing |

| Lender's title insurance premium | Protects the lender's loan position | Usually required on financed purchases |

| Settlement or closing fee | File handling, coordination, document prep, disbursement | Varies by title company |

| Recording fees and taxes | Government filing and transfer charges | Set by state/county/DC rules |

If you want to reduce surprise, separate those categories mentally. The premium itself may be fixed or semi-standardized depending on the jurisdiction. The service experience absolutely is not.

Why buyers in Virginia, Maryland, and DC see different numbers

The DMV is not one uniform closing environment.

Virginia, Maryland, and DC each have their own fee patterns, taxes, customs, and operational differences. That is part of why one buyer hears one number in Arlington and another hears something different in Bethesda or Capitol Hill.

A few practical examples:

- Virginia uses filed title insurance rates, so the premium itself is not usually where comparison shopping changes the number much.

- Maryland also has structured title pricing, but transfer taxes, county taxes, and who customarily pays certain items can change the total picture.

- Washington, DC often produces sticker shock because transfer and recordation taxes can be substantial, and buyers sometimes mistake those government charges for title insurance itself.

That is why the right question is not just "How much is title insurance?" It is also "What exactly is included in my full title and closing estimate?"

Is title insurance worth it if you may never use it?

Yes, especially for an owner's policy.

The fact that you hope never to make a claim does not make the protection less valuable. Title claims are rare compared with the number of policies issued, but when they do happen, they are tied to high-dollar property rights.

Examples include:

- an undisclosed heir asserting an ownership claim

- a prior deed executed incorrectly

- a missed lien or judgment

- a recording error

- fraud in a prior transfer

- boundary or access issues that were not obvious to the buyer

These are not small inconveniences. They can affect your ability to sell, refinance, or fully enjoy the property you thought you owned cleanly.

Can you shop title insurance?

Yes, but shop intelligently.

In Virginia especially, shopping for a radically lower insurance premium is usually the wrong expectation. What you should compare is:

- the quality of the fee estimate

- responsiveness before contract and before closing

- experience with your property type and jurisdiction

- communication with agents and lenders

- the settlement fee and related service charges

- how clearly the company explains your closing numbers

That is where a title company earns its keep.

If one estimate is vague, delayed, or hard to understand, that is not a small issue. It is a preview of the closing experience.

Why the cheapest title company is not always the cheapest closing

A weak title team can cost you more than a modest fee difference.

If they miss a payoff issue, fail to flag an entity-signing problem, mishandle condo documents, or create last-minute wire confusion, the resulting delay can be more expensive than any line-item savings you thought you found.

This is especially true in competitive DMV transactions where lenders, agents, builders, and moving timelines all have to stay aligned.

At Pruitt Title, the goal is not to be mysterious about costs. The goal is to explain the numbers early, keep the file moving, and prevent avoidable friction before it shows up at the table.

The real answer to the cost question

Title insurance feels expensive because:

- it is paid in one shot

- it protects a very large asset

- it includes serious pre-closing risk work

- buyers often confuse the premium with all title-related charges

- the downside of getting title wrong is far more expensive than the premium itself

That does not mean you should accept vague pricing. It means you should get a real estimate from a title company that knows Virginia, Maryland, and DC closings and can explain exactly what you are paying for.

Ready to Take the Next Step?

Learn about title insurance →

Ready to Take the Next Step?

Learn about title insurance →

Ready to Get a Title Quote?

Pruitt Title serves buyers, sellers, and lenders across Virginia, Maryland, and Washington DC. We make closing simple.