You're sitting at the closing table, staring at a stack of documents, and somewhere in there are two line items that look nearly identical: lender's title insurance and owner's title insurance.

Same word. Very different purposes. And if nobody's explained the difference, you're not alone — this is one of the most common questions we get from buyers in DC, Maryland, and Virginia.

Here's the plain-English version.

The Short Answer

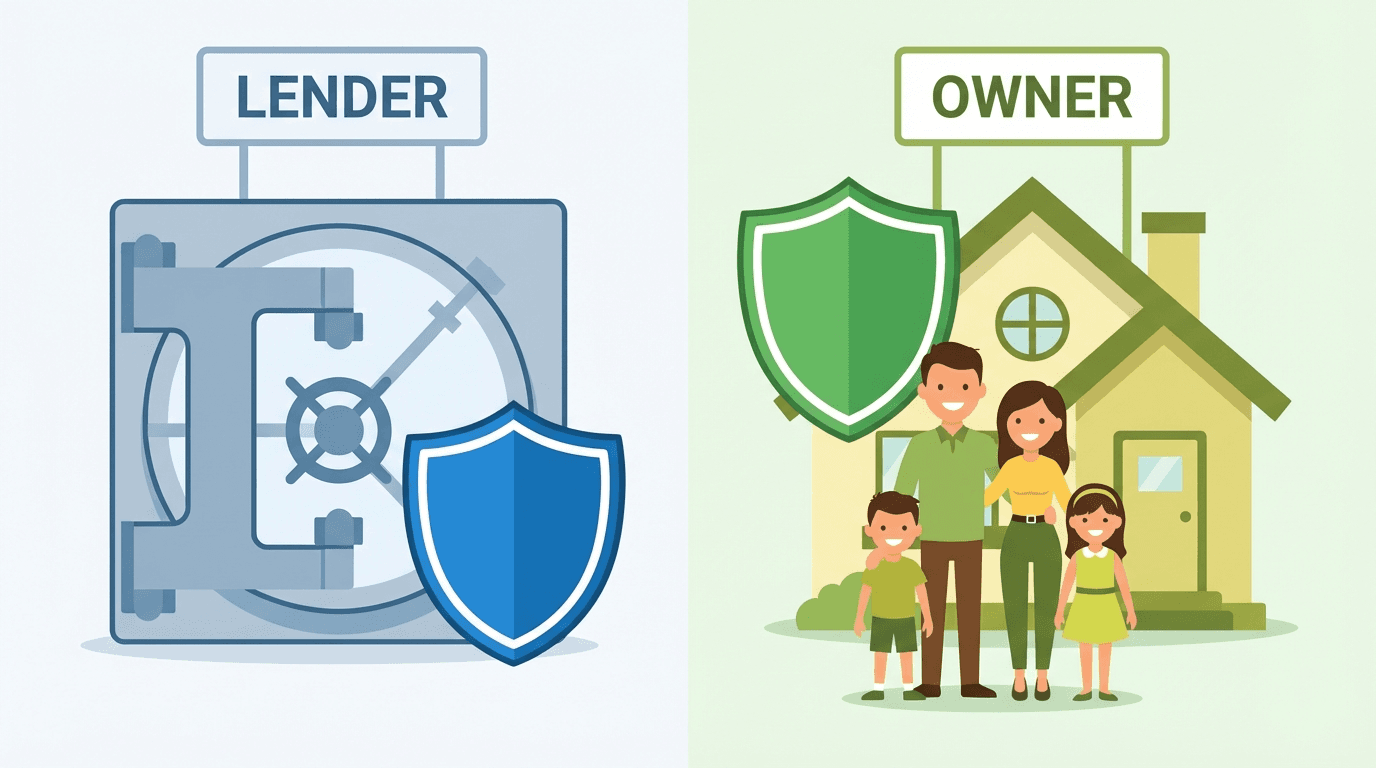

Lender's title insurance protects your mortgage lender if something goes wrong with the property's title.

Owner's title insurance protects "you" — the buyer — if something goes wrong with the property's title.

They're not interchangeable. One is required. The other is optional (but usually worth it).

What Title Insurance Actually Covers

Before we go further, let's make sure we're working from the same foundation.

Title insurance protects against problems with a property's ownership history — things that happened "before" you bought the home. We're talking about:

- Undiscovered liens — a contractor who was never paid, a tax bill that slipped through, a HOA balance the seller didn't disclose

- Ownership disputes — a long-lost heir claiming a stake, a forged signature in the chain of title, a deed that wasn't properly recorded

- Survey errors — encroachments, boundary mistakes, easements nobody knew existed

- Fraud and forgery — identity theft-related title issues are rising in the DMV market right now

Unlike homeowners insurance (which covers future events like fire or flooding), title insurance is a one-time premium that covers your past — everything that happened before you took ownership.

Lender's Title Insurance: The Bank's Protection

When you take out a mortgage, your lender is handing over hundreds of thousands of dollars secured by a property they don't own. They want protection.

Lender's title insurance — sometimes called a loan policy or mortgagee policy — covers the lender's interest in the property up to the outstanding loan balance. If a title defect surfaces and ownership gets disputed, the lender's claim gets covered.

Key facts about lender's title insurance:

- Required in virtually every transaction with a mortgage. If you're financing your purchase, you're buying lender's coverage. This is non-negotiable.

- Covers the lender, not you. You're paying for it, but the policy protects the bank's investment — not your equity.

- Coverage decreases over time. As you pay down your mortgage, the lender's exposure shrinks, and so does the coverage.

- One-time premium paid at closing. No monthly payments — it's folded into your closing costs.

In Virginia and Maryland, lender's title insurance is calculated based on your loan amount. On a $600,000 loan, expect to pay roughly $1,000–$1,500 for the lender's policy, though exact rates vary by state and title company. Title insurance rates are filed with the state — your title company can provide an exact quote based on your transaction.

Owner's Title Insurance: Your Protection

Here's the thing most buyers don't realize until it's too late: lender's title insurance does nothing for you as the homeowner.

If a title defect surfaces — an old lien, a missing heir, a recording error — and you end up in a legal dispute over your property, the lender's policy pays the bank. You're on your own.

That's where owner's title insurance comes in.

An owner's policy protects your equity in the property — the difference between your home's value and what you owe. It covers your legal defense costs if someone challenges your ownership, and it pays out if a covered claim results in you losing all or part of your property.

Key facts about owner's title insurance:

- Optional in most states, including Virginia, Maryland, and DC. But optional doesn't mean unimportant.

- Covers you — not the lender. The policy protects your ownership interest for as long as you own the property.

- Coverage stays constant (or grows). Unlike the lender's policy, owner's coverage doesn't decrease as you pay down your loan. Enhanced policies actually increase with home value appreciation.

- One-time premium paid at closing. Usually a few hundred dollars more than the lender's premium.

- Transfers to your heirs. When the property is inherited, the coverage extends to family members who receive it.

In Virginia, the owner's policy premium is typically modest relative to the purchase price — often $1,500–$2,500 on a $700,000 home — and it covers you for the entire time you own the property.

Ready to Take the Next Step?

Learn about title insurance →

Ready to Take the Next Step?

Learn about title insurance →

DMV title services: Vienna, VA | Springfield, VA | Bethesda, MD

Ready to Get a Title Quote?

Pruitt Title serves buyers, sellers, and lenders across Virginia, Maryland, and Washington DC. We make closing simple.